Analysis of Salary Growth Rate assumption adopted by NSE 50 Companies

Salary growth rate and discount rate are the two most important assumptions adopted while performing actuarial valuation of salary based employee benefit schemes such as gratuity, earned leaves, pensions, etc. The importance of these assumptions is underscored by sheer sensitivity of the liability to these assumptions - a 1% change in any of these assumptions e.g. an increase in salary growth rate from 6% p.a.to 7% p.a. can have an impact of around 10% increase in the liability.

Also, salary growth rate assumption is often a point of discussion (perhaps debate) between auditors and the management, with auditors looking at the salary growth rates over the last few years and questioning something which is essentially a long term assumption.

As actuarial consultants providing advice and actuarial valuation services, we often receive request from our clients and their auditors to provide benchmarks against which they can validate their actuarial assumptions. It is in this backdrop that we undertook the research of actuarial assumptions, methodologies, practices and reporting adopted by NSE 50 companies.

Why NSE 50 Companies?

The companies considered for this research are amongst the largest corporate houses in India. They are also amongst the ones which are audited by the biggest audit firms in the country. It is therefore not unreasonable to expect the practices adopted by these companies to be amongst the best in the industry.

Quick Overview of the findings

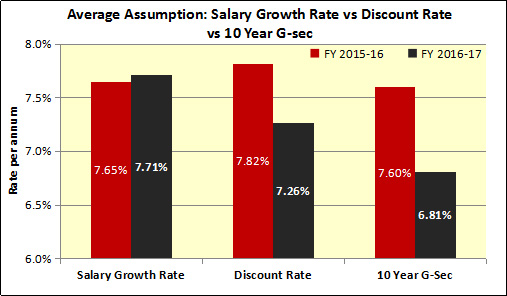

Following graph shows the average salary growth rate assumed and the average discount rate used by the NSE 50 companies and their comparison with 10 year Government bond yields over the last two financial years:

Source: Annual reports of various companies and www.investing.com. The details captured for each company can be accessed by http://www.kpac.co.in/images/Salary-Sectoral-Research.pdf.

Following are the main findings of our analysis of salary growth rate and discount rate assumptions of the NSE 50 companies over the last couple of years:

- As can be observed from the above chart, it can be seen that the absolute level of average Salary Growth Rate assumption for NSE 50 Companies over the past two financial years was more or less constant (7.71% p.a. as at 31 March 2017 vs 7.65% p.a. as at 31 March 2016).

- The average discount rate assumption fell sharply from 7.82% p.a. as at 31 March 2016 to 7.26% p.a. as at 31 March 2017. This fall of 55 bps was driven by fall in yields on government bonds. As can be seen from the above table, the yield on benchmark 10-year government bond fell by about 80 basis points during FY2017 whereas the fall in yields on government bonds was different for bonds of different terms.

- For the first time in the past many years, the average salary growth rate assumption was observed to be higher than the average discount rate assumption. This signifies relative strengthening of salary growth rate assumption over the last few years. Salary growth rate analysis of NSE 50 companies for earlier years can be accessed by clicking here: Â Â Â Â http://www.kpac.co.in/images/Salary-Growth%20Rate-NSE-50-Companies.pdf

- It should be noted that the discount rate, representing yields on government bonds, is closely linked to the market’s long term expectation of inflation in the economy. Similarly, the salary growth rate is also likely to be at least as much as the inflation over the long term (to protect the real level of income). Thus, salary growth rate and discount rate are expected to be positively correlated with each other. As a result of this relationship, a fall in discount rate, which is not accompanied by a fall in salary growth rate assumption, can be regarded as strengthening of economic assumptions used in actuarial valuations.

- Despite the above relative strengthening during FY2017 and the absolute strengthening observed over the last few years, we still believe that the salary growth rate assumption adopted by some of the NSE 50 is lower than the actual increments being given by them to their employees. Thus, in our view, there is scope for such companies to strengthen their salary growth rate assumption and with the bond yields rising in current financial year (FY2018), the Companies may have the opportunity to strengthen their assumptions. Refer below for further details.

- Two Companies have salary growth rate assumption varying for various categories of employees (rather than a single rate). Refer below for further details.

- Four Companies have salary growth rate assumption varying by year of projection (rather than a single rate for all the future years). Refer below for further details.

Application of Salary Growth Rate

Most of the Companies stick to a single assumption for salary growth rate in their valuation (e.g. assumption of 6% per annum for all future projection years). However, companies could consider varying the assumption on the following basis:

- Varying Salary Growth Rate by year of projection

Varying salary growth rate assumption by year of projection means assuming salary growth rate to be different in different future years. For example, the salary growth can be assumed to be 10% p.a. for next 3 years of projection and 8% p.a. thereafter. As indicated above, 4 NSE 50 companies (Asian paints Limited, Dr. Reddy’s Laboratories Limited, Hero MotoCorp Limited and Lupin Limited) adopted such an assumption for their actuarial valuation of employee benefit as at 31 March 2017.

This approach gives the company an advantage that it could reflect the currently higher (or lower) salary growth rate expected over the next few years whilst sticking to its structural view over the long term. Also, it may help build a consensus with the auditors who may be questioning the salary growth rate assumption based on the salary growth rates actually given to employees over the last two to three years.

You can refer to one of our earlier articles on this approach by clicking on the following link:

http://www.kpac.co.in/kc/12/salary-growth-rate-varying-by-year-of-projection.html

- Varying Salary Growth Rate by Category of employees

In this case, the salary growth rate assumption is to vary on the basis of employee classification. For example, employees can be classified as management employees and non-management employees and different rates of salary growth can be assumed for both the groups.

Doing so helps the organization in setting a more realistic liability as generally it is seen that the hike in the salary varies over classes of employees within an organization and thus assuming the same rate of increment for all the employees may prove to be biased.

Outlook and Recommendations

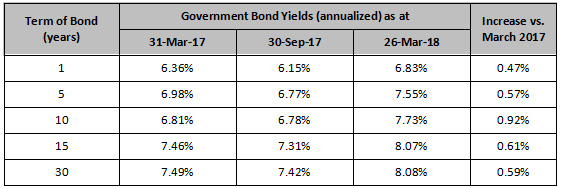

Yields on government bonds have been rising over the last couple of months, driven by likely upward trajectory of inflation in the near term, fiscal slippage, impact of HRA increases by State Governments, setting of MSPs for Kharif crops (as proposed in budget FY19), fiscal and monetary policy changes by advanced economies.

The following table shows comparison of yields on government bonds of various terms as at 31 March 2017, 30 September 2017 and 26 March 2018:

As can be seen from above, the bond yields have risen significantly during the current financial year. This will result in higher discount rates being used in actuarial valuations of employee benefits, resulting in lower expenses. Therefore, Companies looking to strengthen their salary growth rate assumption can use this opportunity to do the same.

Concluding Thoughts

Overall, the average salary growth rate assumption has risen over the last few years before stabilizing around 7.7% as at the end of 31 March 2016 and 31 March 2017. However, we believe that the salary growth rate assumption adopted by some of the organizations amongst NSE 50 companies is still lower than the actual salary growth rates being experienced by them. With the discount rates expected to rise during the current financial year, we expect such companies to use this opportunity to strengthen their assumptions used in actuarial valuations. If such strengthening happens, we may observe an increase in average salary growth rate assumption during FY2018.

I thank you for reading this note and welcome any comments or recommendations or observations you may have on the subject. You can direct those to the email address mentioned below.

Khushwant Pahwa, FIAI, FIA, B Com (H)

Founder and Consulting Actuary

KPAC (Actuaries and Consultants)

k.pahwa@kpac.co.in

www.kpac.co.in