Past Service Cost – AS (AS15) vs. IFRS (IAS19) and IND AS19 vs. US GAAP (ASC715)

When performing an actuarial valuation of employee benefit scheme (such as gratuity valuation), we perform movement analysis of the liability i.e. reconcile opening PVO (Present Value of Obligation) to the closing PVO. One important item which figures out in the reconciliations is Past Service Cost.

Past service cost is the change in the present value of the defined benefit obligation for employee service in prior periods, resulting in the current period from the introduction of, or changes to, post-employment benefits or other long-term employee benefits. Past service cost may be either positive (where benefits are introduced or improved) or negative (where existing benefits are reduced).

Past service cost arises when an enterprise introduces a defined benefit plan or changes the benefit plan or changes the benefits payable under an existing defined benefit plan. Treatment of Past service cost differs from one standard to another. It is important to study these differences in the requirements of various standards in light of the much anticipated change in gratuity limit from ten lakhs to twenty lakhs, which will be treated as Past service cost.

It should be noted that the bill to increase gratuity limit has been tabled in the Lok Sabha on 18 December 2017 and can be accessed by clicking on the following link:

http://www.prsindia.org/billtrack/the-payment-of-gratuity-amendment-bill-2017-5002/

In this note, we bring out the requirements of various standards for recognition of Past service cost for post-employment plans such as gratuity, pensions etc.

Indian GAAP - Accounting Standard (AS) 15

Para 94 of AS 15, which talks about recognition of Past service cost, reads as under:

“An enterprise should recognize past service cost as an expense on a straight-line basis over the average period until the benefits become vested. To the extent that the benefits are already vested immediately following the introduction of, or changes to, a defined benefit plan, an enterprise should recognize past service cost immediately.â€

As can be inferred from above, the increase in Present Value of Obligation (“PVO†or “liabilityâ€) due to increase in gratuity limit shall be recognised as follows:

- Increase in PVO attributable to employees who have completed vesting criteria (usually 5 years) shall be recognised immediately in the statement of Profit and Loss;

- Increase in PVO attributable to employees who have not completed the vesting criteria shall be recognised in the statement of Profit and Loss over the remaining period to the vesting.

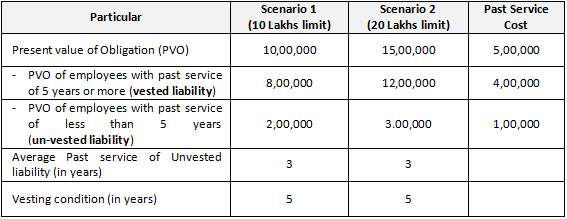

The following simple example demonstrates the treatment of Past Service Cost arising due to increase in Gratuity limit under AS15:

In the above example, the Present Value of Obligation increases from Rs. 10,00,000 to Rs. 15,00,000 due to the increase in limit. Thus, the total Past Service Cost is Rs. 5,00,000.

Out of the total Past service cost of Rs. 5,00,000, the Past service cost of Rs. 4,00,000 arising in respect of employees with past service of 5 years or more will be recognized as an expense immediately in the statement of Profit or Loss, whereas, past service arising in respect of employees with service of less than 5 years will be recognized as an expense in Profit or Loss Statement over 2 years (i.e. the remaining period to the vesting).

IFRS - International Accounting Standard (IAS) 19 / Indian Accounting Standard (IND AS) 19

Para 103 of IAS 19 / IND AS 19, which reads as under, requires Past service cost to be recognized immediately as an expense in the statement of Profit or Loss:

“An entity shall recognize past service cost as an expense at the earlier of the following dates:

- when the plan amendment or curtailment occurs; and;

- when the entity recognizes related restructuring costs or termination benefits

Thus, in the above example, the entire Past Service Cost of Rs. 5,00,000 will be immediately recognised as an expense in the statement of Profit and Loss.

US GAAP - Accounting Standard Codification (ASC) 715

ASC 715-35-15 requires past service cost, including costs related to vested benefits, to be initially recognized in Other Comprehensive Income (OCI) with subsequent charging to the net periodic post-retirement benefit cost.

This subsequent charge to the net periodic benefit cost should be determined, at a minimum, by assigning an equal amount of past service cost to each remaining year of service to full eligibility date of each plan participant active at the date of the amendment who was not yet fully eligible for benefits at that date. The portion of prior service cost to be recognized in net periodic postretirement benefit cost in each of those future years is weighted based on the number of those plan participants expected to render service in each of those future years.

It should be noted that the above is only the minimum amount of Past Service Cost that should be charged to the Net Periodic Benefit Cost. ASC 715-35-18 also permits the reporting entity to reduce the complexity and detail of the computations required by consistent use of an alternative approach that more rapidly amortizes the prior service cost recognized in accumulated other comprehensive income. Thus, an entity can also choose to recognize / charge the entire past service cost immediately as it arises.

Conclusion

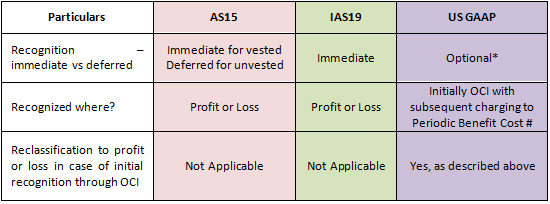

The following table summarizes the provisions discussed above:

* Minimum recognition prescribed as per ASC715. The Company can choose to recognize all immediately or any other systemic approach provided certain criteria, mentioned above, are met.

# OCI – Statement of Other Comprehensive Income

In addition to above, it should also be noted that if any entity is having unrecognized past service cost in the balance sheet on the date of transition from earlier iGAAP to IFRS-converged Ind ASs (i.e. from AS15 to Ind AS19), then it will become a transition item with the equity of the entity being adjusted (lowered) in preparation of opening Ind AS balance sheet.

I hope you found the above note useful. I thank you for reading this note and welcome any comments or recommendations or observations you may have on the subject. You can direct those to the email address mentioned below.

Khushwant Pahwa, FIAI, FIA, B Com (H)

Founder and Consulting Actuary

KPAC (Actuaries and Consultants)

k.pahwa@kpac.co.in

www.kpac.co.in