Gratuity Valuation: Impact of limit of Rs. 10 lacs

From Actuary's Desk

Gratuity Valuation: Impact of limit of Rs. 10 lacs

Any actuarial valuation requires three kinds of inputs - the data, assumptions and the benefit structure. Whilst most of the subjectivity lies in the determination of assumptions and whilst most of the operational errors are encountered in compilation of data, the benefit structure to be valued is also capable of throwing surprises. One such item in actuarial valuation of gratuity benefit is whether the limit of Rs. 10 lacs should be applied or not.

We have often observed that certain companies, usually younger companies which are yet to experience actual gratuity pay outs or relatively smaller companies, are not sure of whether to get actuarial valuations done with or without the limit of Rs. 10 lacs. In fact, many do not fully appreciate that having or not having a limit on gratuity payout can have a significant impact on the actuarially valued liability.

In this article, we have attempted to examine the impact of having a limit on gratuity benefits on the actuarially valued gratuity liability of a Company

What does the Payment of Gratuity Act, 1972 say?

Section 4 of the Payment of Gratuity Act, 1972, lays down the amount of gratuity benefit an entity needs to pay to its employees. Sub section (3) of Section 4 of the Act prescribes the maximum limit on the gratuity as:

“(3) The amount of gratuity payable to an employee shall not exceed ten lakh rupees.â€

The Act, however, does not stop an entity from paying a higher benefit than that stipulated in Section

4. This aspect is clarified in Sub Section (5) to Section 4, which reads as under:

“(5) Nothing in this section shall affect the right of an employee to receive better terms of gratuity under any award or agreement or contract with the employer.â€

Why does the issue arise?

The issue relating to gratuity limit in actuarial valuations typically arises because of two reasons:

Firstly, some companies do not have a written gratuity policy (as the actual gratuity payouts are made as per the Payment of Gratuity Act, 1972) or even where there is a policy, it may be silent on whether the ceiling of Rs. 10 lacs is applicable or not. In such cases, the question of whether the limit shall be applied or not gets answered when some senior employee leaves whose gratuity amount is significantly different when calculated with or without limit. Until such time, the Companies get the gratuity valued with or without limit without having clarity of what is eventually going to happen on the policy side.

Second reason why we have observed inconsistencies in the company policy / practice and what is actually considered in actuarial valuation is that companies focus on communicating the assumptions and providing the data to the actuary for valuation. However, explicit communication on whether the valuation is required with limit or without does not always happen.

For both the above reasons, the valuation may not reflect the correct position of the company with regards to the limit and hence the liability may be over or undervalued compared to what it should be if the policy / practice of the company were to be strictly allowed in the actuarial valuation.

In this back-drop, we now look at the impact of limit on actuarial valuation with the help of a simple example.

Impact of limit on actuarial valuation - a worked example!

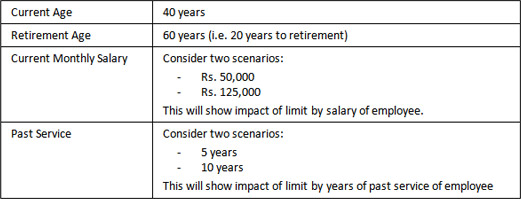

Let us consider an employee with the following inputs for valuation of gratuity as on the valuation date:

The salary growth rate and discount rate have been assumed to be 7.50% per annum and 8.00% per annum respectively. Further, for sake of simplicity, it has been assumed that there would be no resignations and deaths and hence the employee will leave the organization only on retirement.

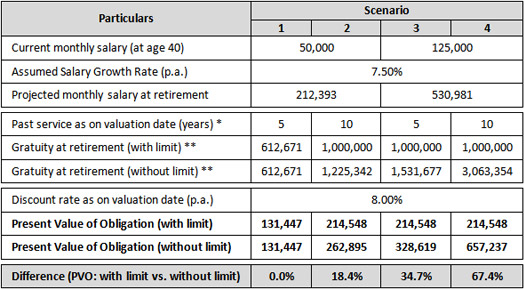

‘Projected monthly salary at retirement’ has been calculated by considering the salary escalation rate of 7.50% p.a. up to the retirement date. The present value of obligation has been calculated as the expected future payments required to settle the obligations resulting from employee service in current and prior periods assuming a discount rate of 8% p.a.

The table below shows the working of gratuity liability for this example:

* Please note that we are required to recognize liability in the books of accounts only in respect of service rendered by the employee up to the date of valuation.

** Calculated using the standard gratuity formula of 15/26 * Salary * Completed years payable, with or without limit.

As can be seen from the above table, in case the salary is higher, the employee is more likely to hit the limit and hence the difference in the liability calculated with or without limit is higher. Similarly, in case of employees with higher past service, the projected gratuity amount is higher and hence the difference is higher.

Thus, getting an actuarial valuation of gratuity benefit done with or without limit can have a significant impact on the liability amount. The impact, for the company as a whole, may not be as much as is coming out of the above example for reasons such as:

- Not all employees will be likely to hit the ceiling and hence whether the valuation is carried out with or without limit will make no difference to their liability;

- The above example does not consider attrition and deaths as is typically the case in an actuarial valuation. Attrition and deaths mean that employees are expected to leave the organization earlier, before the gratuity ceiling actually bites / hits.

Nevertheless, we have seen cases of gratuity valuations where a difference of more than 10% has been observed between the liability calculated with or without limit being applied in the projection.

Conclusion - what should you be mindful of?

Having understood the impact of having or not having a limit (on benefits) on your ultimate liability, it is important that you then consider the following:

- Be sure of your policy: It is important that you are sure of the gratuity policy being followed in your organization before getting the valuation done. Where there is no written policy, looking at past practices also becomes important factor in determining whether the limit should be applied in the valuation or not.

- Ensure that the policy is correctly captured in report: Make sure that you clearly communicate whether the valuation is required with limit or without limit. Also, look at the actuarial valuation report carefully to ensure that your policy is correctly reflected in the report.

- Look at employee wise liability: And to be completely sure, you can ask your actuary to share the employee wise liability. Where the limit is applicable, no employee should have a liability of more than Rs. 10 lacs.

I trust you will find the observations and assertions in this note useful. I thank you for reading this note and welcome any comments or recommendations or observations you may have on the subject. You can direct those to the email address mentioned below.

Khushwant Pahwa, FIAI, FIA

Founder and Consulting Actuary

k.pahwa@kpac.co.in

+91-9910267727